Before we dive into power, you have to understand where it sits in the broader context. There are three major commodity categories: energy (e.g. power, crude oil, natural gas), agriculture, and metals. All commodities have some basic properties in common, which set them apart from other asset classes.

Equities vs. commodities

Equities and commodities are different from each other in two major ways.

First, a stock doesn't have any sort of forcing function collapsing the price to its fundamental value. A commodities contract, in comparison, has a fixed settlement date. On the settlement date, someone will come and physically buy or sell that tradeable commodity. If the corn is too expensive, they're not going to buy it. Prices must collapse to reality.

Second, the underlying companies that equities represent have various relationships with each other that are sometimes hard to untangle, such as contracts, shared customers, supply chains, and so forth. Commodities feed into each other in a much more straightforward way. A wellhead drilled into the ground results in some amount of crude oil and some amount of natural gas (mostly methane). Crude oil is great because it can be shipped easily all over the world. Its global market means that prices abroad impact us here in the US, hence the widespread concern around the closure of the Strait of Hormuz. That crude oil has a market price, and refineries buy it to produce distillates: petroleum products like gasoline, diesel, and jet fuel. That's the same gasoline that you buy at the gas pump.

If a well produces almost no oil, we call it a dedicated gas well, and that's where the majority of domestic natural gas comes from. Natural gas cannot be shipped in its raw form so easily, but you can cool it and ship it in the form of liquefied natural gas (LNG). The prices for natural gas abroad have lately far exceeded the prices in the US, so we export as much as we can. As a result, natural gas prices abroad don't impact us here in the US as much in the short-term. In a simplified sense, the natural gas we have here in the US is the supply that couldn't be physically exported. Natural gas is consumed by some industrial use cases (e.g. chemical manufacturing), residential-commercial (e.g. heating your home), and power - the focus of this primer.

The system balance equation

The commodities market has to "solve" in a particular way at each location:

Supply = Demand + Net Exports + Change in Storage

Supply is the amount that the local merchants need to produce. Demand is how much is consumed at a specific location. Net exports are the units exported from a region minus whatever was imported. Change in storage is the quantity stored minus the amount drawn from storage. This equation must hold true at every location in the entire world. There are additional constraints:

- You can only transfer so much supply from one point to another (only so many trucks/ships available, or a power line can only support so much transmission - more on this later)

- You can't draw more from storage than you put in, and you can only store a maximum amount of supply at a given time

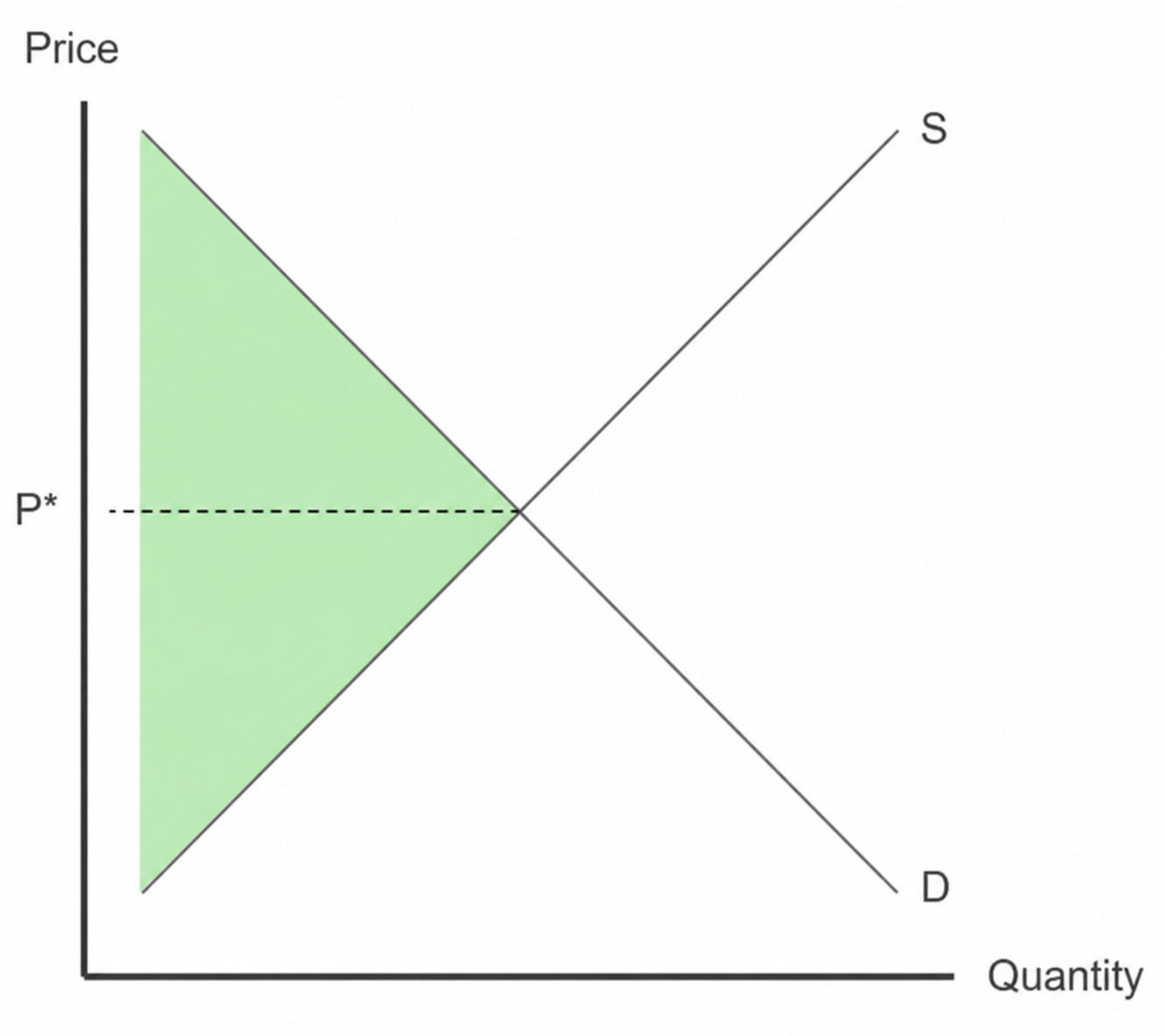

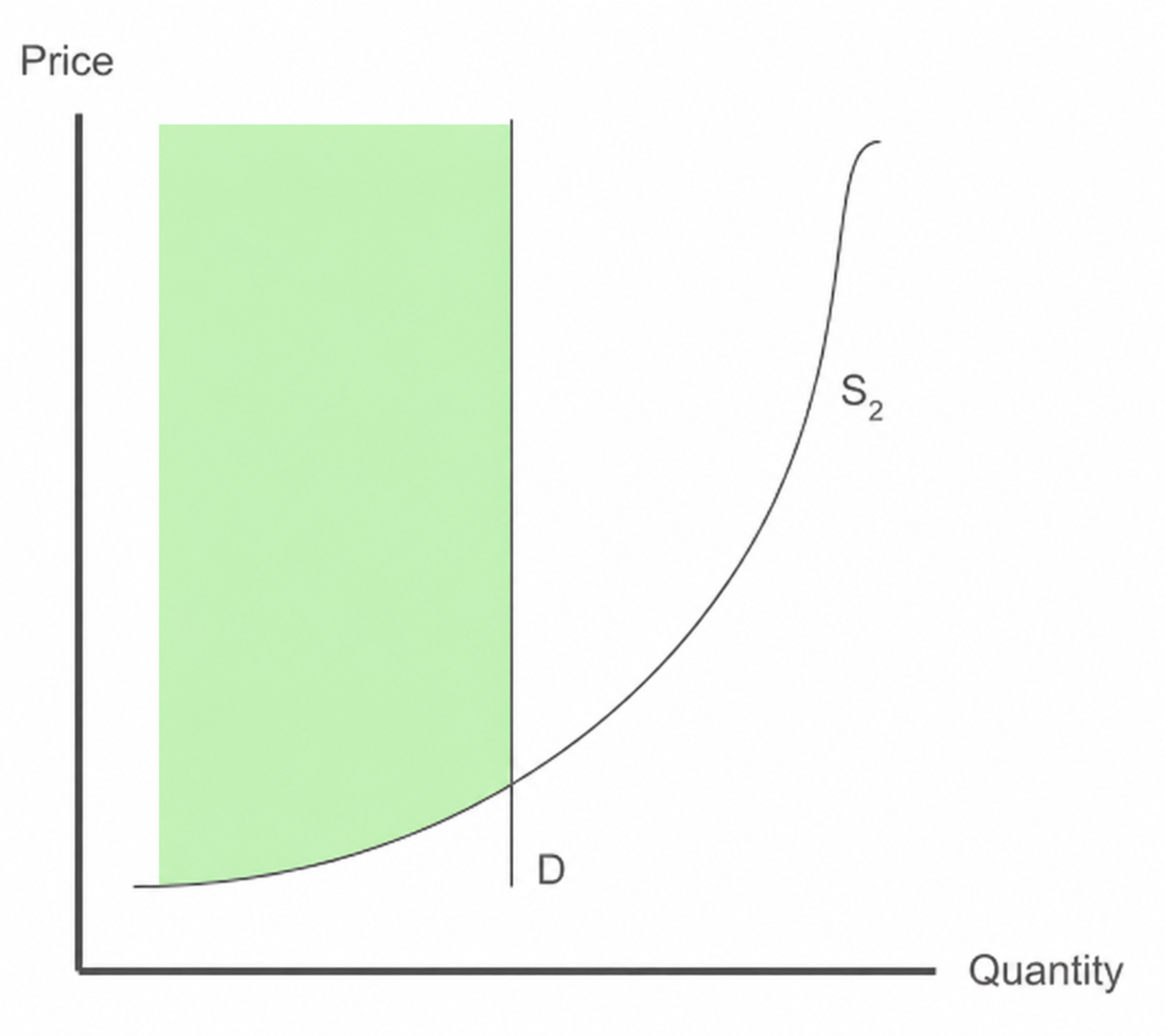

If you know basic economics, you'll understand that each of the above variables is a function of price. Price is the amount of money that consumers pay and suppliers receive. If price increases at a location, then it becomes economical to produce more supply there (less efficient producers can now serve the demand without losing money), and the local demand goes down. Of course, it'll also decrease net exports (if there were any at all) and incentivize more supply to come out of storage (if any exists). The price will change everywhere until the system "balances."

At any given time, all of the units that are sold, whether the "first" unit sold or the "last" one, are sold at the same price. You might think that if it's really cheap for a supplier to produce goods, maybe they'd try to charge a little less. But in a competitive market, you don't personally get to "pick" the price at which you sell. This is a critical assumption for how commodities pricing works. So what determines that market price?

If we were to produce 1 additional unit of supply after demand/storage/exports are met, we would pick the cheapest producer that is not at full capacity. The cost of producing that additional unit of supply is called the "marginal cost." In a competitive market, the market price that everyone sells at is exactly equal to that marginal cost. Note that if you're the producer who provided the last unit of supply, you make $0 of profit; the price is equal to your marginal cost. This property is called "marginal pricing". It will be extremely relevant for power pricing.

A simple justification for why this is true: Let's pretend like that marginal producer refuses to sell at their marginal cost. They're only willing to sell for higher. The issue is that the market is competitive. There's another supplier who's going to undercut that attempted market price. This will keep happening until the market price is exactly equal to the marginal cost of the cheapest producer that can offer the additional unit of the supply. If the price were lower, then it would be uneconomical for anyone to supply that unit.

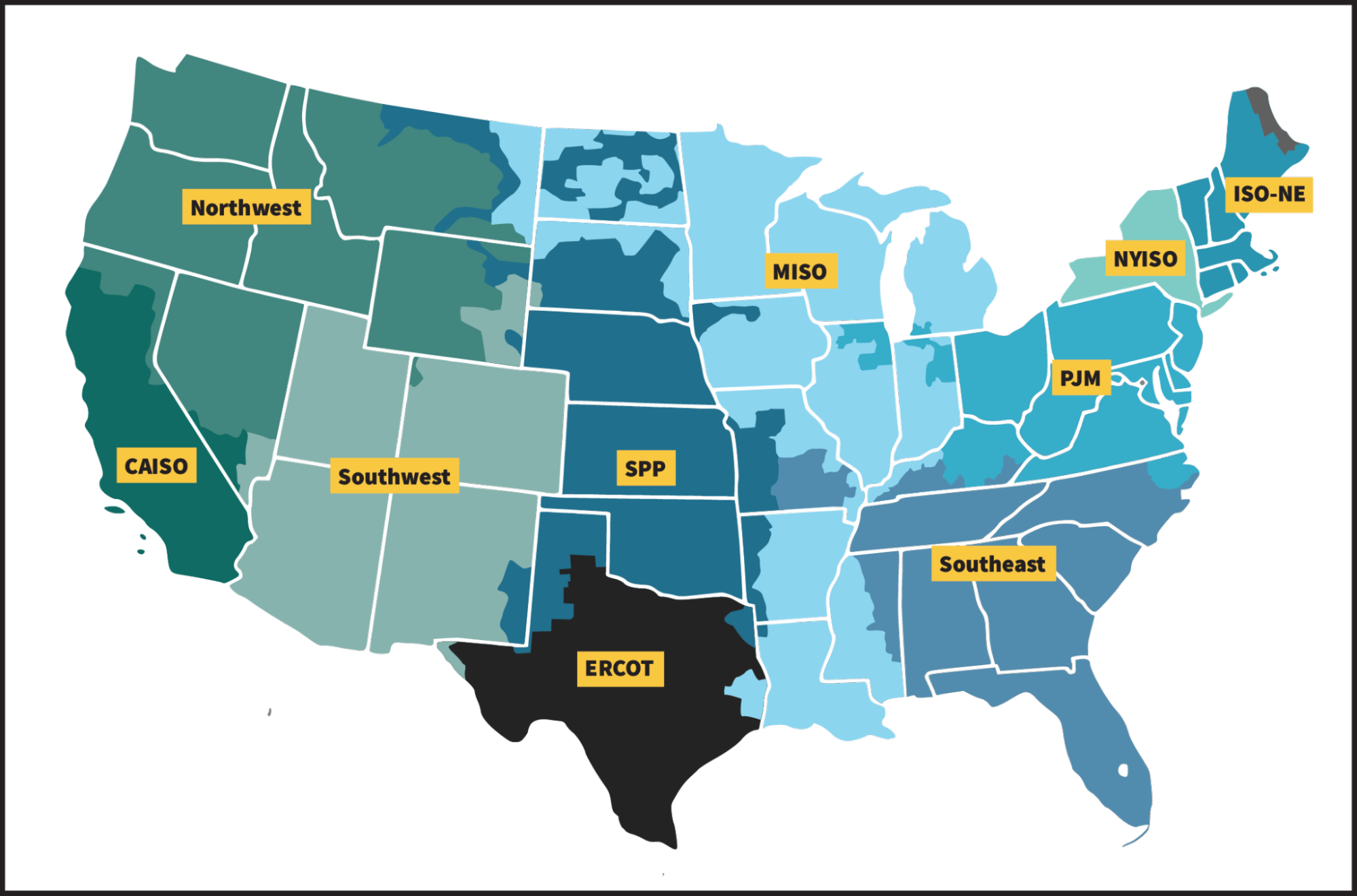

Power is special

Power is injected into or withdrawn from the grid at physical "buses". These buses are numerous and are spread out within every city in the US. They're all connected via transmission lines.

To rewrite the equation above in electricity terms for a specific location, which could be a physical power bus, a whole city, or an entire state:

Generation = Power Consumption + Net Power Exports + Change in Storage + Losses

Generation is the electricity produced by power plants at that location, which we'll dive into later. You're probably already familiar with power consumption, since you consume power to turn on your lights.

Exports/transmission occurs over a physical power line. When you push power through it, it heats up. That heat means it loses a little bit of power along the way. The metal also expands when it's hot. The more power you push through, the hotter the line gets, and the more it expands. If the power line expands too much, the power line could droop too low and light a tree on fire. As a result, each transmission line comes with a "rating." That's the maximum amount of power that can be pushed through that line.

Storage, in this case, refers to batteries, pumped storage, compressed air, and so forth. Like I mentioned, losses occur when power is transmitted over a power line.

There's one last thing that makes power different from the other commodities. If I buy 1000 barrels of oil, I can literally take physical delivery of those barrels of oil. If I buy 1 megawatt-hour (MWh) of power on the market, that doesn't necessarily mean I can just go and plug 1000 GPUs into the wall and start consuming 1 MW for an hour.

That's because the power market has a central authority called the independent system operator (ISO). They take in all the bids from local utilities (load serving entities) and all the offers from local power plants, and they compute the efficient market price at each location, plus intended generation and flows. Then throughout the day, they tell each generator how much power they need to produce based on how much consumption they anticipate at each location. (In some regions, there is no ISO, but an entity called a balancing authority still ensures the grid stays stable.)

The reason we need the ISO is to keep the grid balanced. When you draw a ton of power from the grid, you lower its frequency. The opposite holds true if you're pumping power in. But these generators are like $100M+ machines that are rotating at the exact speed to produce power at the right frequency (60 Hz). We'll talk more about that rotation later, but all you need to know right now is that if the frequency of the grid differs from the correct frequency, it can cause serious damage to the generators.

In extreme cases, if someone is really consuming too much power, the balancing authority will cut them off. Sometimes, people aren't even trying to screw up the grid, but there just isn't enough supply to meet demand, like if major generators go on outage, or if it's a really cold winter and everyone is consuming a lot of power. To spare the generators, we're forced to resort to brownouts or blackouts, where parts of the grid are cut off.

It might seem like as a generator, you're subject to the day-to-day whims of the ISO, who tells you exactly how much you're going to get paid. That said, there are a variety of ways to trade power and hedge a physical plant if you own one, which we'll get into. Most data center operators hedge in some way.